Payroll taxes explained is one of the most important topics every employee should understand because the difference between gross earnings and take-home pay often causes confusion. When people receive a paycheck for the first time or even after years in the workforce they frequently wonder why the amount deposited into their bank account is significantly lower than their salary. The answer lies in payroll taxes, paycheck deductions, payroll withholding, employee benefits, and other required contributions that support both personal obligations and public programs.

Every payroll system is designed to calculate earnings, apply legally required deductions, and distribute funds appropriately. While many workers focus only on their net pay, understanding gross pay vs. net pay provides a much clearer picture of where every dollar goes. Payroll deductions may include taxes, retirement savings, health insurance premiums, and other employer-sponsored benefits.

Beyond affecting individual paychecks, payroll systems also play a critical role in funding retirement programs, healthcare initiatives, unemployment protections, and government services. At the same time, payroll rules, contribution rates, and withholding requirements vary by country, employer, and jurisdiction, and they may change over time. Learning how payroll deductions work therefore improves financial literacy, strengthens budgeting skills, and helps employees make more informed personal finance decisions throughout their careers.

Understanding Payroll Taxes and How They Work

At their core, payroll taxes are mandatory deductions connected to employment income. Employers calculate these amounts through a payroll system before employees receive their wages. Depending on the country, payroll taxes may finance retirement programs, healthcare systems, unemployment insurance, disability benefits, or other public services.

Employee payroll taxes generally involve deductions withheld directly from wages. Employers, meanwhile, often have their own separate tax obligations that employees never see on a pay stub. This distinction explains why payroll costs for employers usually exceed an employee’s gross salary.

Most payroll systems follow a similar process:

- Calculate gross earnings.

- Apply required payroll withholding.

- Deduct applicable taxes and approved benefits.

- Calculate net pay.

- Remit required payments to the appropriate government agencies.

Although the overall process appears straightforward, every country establishes its own contribution rates, exemptions, reporting rules, and payroll compliance requirements. Consequently, employees working in different jurisdictions may notice significant differences in paycheck deductions even when earning similar salaries.

Modern payroll platforms automate much of this work, reducing calculation errors while helping employers comply with changing tax regulations. Nevertheless, employees benefit from understanding the process because reviewing payroll information regularly makes it easier to identify discrepancies and ask informed questions when necessary.

Gross Pay vs. Net Pay: Why Your Paycheck Looks Smaller

Understanding gross pay vs. net pay is essential for interpreting every paycheck accurately.

Gross pay represents total earnings before deductions. It may include regular wages, overtime, commissions, bonuses, or other taxable compensation depending on employer policies.

Net pay, by contrast, is the amount employees actually receive after payroll tax deductions, income tax withholding, retirement contributions, insurance premiums, and other authorized deductions have been applied.

Several factors influence the gap between gross and net pay, including:

- Payroll taxes

- Income tax withholding

- Retirement contributions

- Health insurance premiums

- Flexible spending or similar benefit programs

- Court-ordered deductions where applicable

Many employees mistakenly believe employers simply reduce pay arbitrarily. In reality, employers generally act as withholding agents, collecting required amounts and transferring them to government agencies or benefit providers.

Employer-paid payroll taxes deserve particular attention because they do not reduce an employee’s paycheck directly. Instead, they represent additional employment costs borne by the employer. As a result, an employer’s total compensation expense often exceeds an employee’s visible salary.

Understanding these distinctions improves budgeting because employees learn to estimate realistic take-home income rather than relying solely on advertised salaries.

Breaking Down Every Major Payroll Deduction

Every paycheck contains several deductions serving different purposes. Some are mandatory under employment laws, while others reflect voluntary benefit elections chosen by employees.

Payroll taxes help finance public programs that may include retirement systems, healthcare initiatives, unemployment protection, and other government services. Income tax withholding represents estimated income taxes collected throughout the year based on applicable tax rules.

Retirement contributions help employees save for future financial security, while insurance deductions support access to healthcare and other workplace benefits.

The following comparison summarizes several major paycheck deductions.

| Payroll Deduction | Purpose | Who Pays |

|---|---|---|

| Payroll Taxes | Fund public social programs | Employee and employer (varies by jurisdiction) |

| Income Tax Withholding | Prepay estimated income tax | Employee |

| Retirement Contributions | Build long-term retirement savings | Employee, employer, or both |

| Health Insurance Premiums | Support healthcare coverage | Employee, employer, or both |

| Other Voluntary Benefits | Finance optional workplace benefits | Employee |

Although these deductions appear together on a pay stub, they perform very different functions. Confusing them often leads employees to misunderstand why their take-home pay changes over time.

For example, increased retirement contributions reduce current net pay but may significantly improve long-term financial security. Likewise, benefit deductions often purchase valuable insurance coverage that protects against unexpected medical or financial expenses. Looking at deductions individually rather than collectively provides a much clearer understanding of compensation.

Payroll Taxes vs. Income Tax Withholding

One of the most common sources of confusion involves the difference between payroll taxes and income tax withholding.

Payroll taxes generally support designated public programs tied directly to employment. In many jurisdictions, these contributions finance retirement systems, healthcare, unemployment insurance, or similar national programs.

Income tax withholding works differently. Rather than funding a specific employment program, employers withhold estimated income taxes based on tax regulations and employee withholding information. Actual income tax liability is typically reconciled later through an annual tax filing process where applicable.

In countries that use FICA taxes, Social Security taxes and Medicare taxes fall under employment-related payroll withholding rules. Other countries operate different systems with different names, contribution rates, and benefit structures.

Because both payroll taxes and income tax withholding reduce take-home pay, employees frequently assume they represent the same deduction. They do not. Each serves a separate policy objective, follows different calculation rules, and may affect annual tax outcomes differently.

Understanding this distinction helps employees interpret payroll information more accurately while avoiding common misunderstandings during tax season.

Common Payroll Tax Myths

Payroll deductions remain one of the least understood aspects of personal finance. Several misconceptions continue to circulate despite modern payroll transparency.

Common myths include:

- Employers keep payroll taxes.

- Every paycheck deduction is a tax.

- Higher earnings always reduce overall take-home income.

- Payroll taxes and income taxes are identical.

- Payroll deductions never change.

In reality, employers generally remit required payroll tax deductions to government authorities rather than retaining them. Similarly, many paycheck deductions finance insurance coverage, retirement savings, or other employee benefits instead of taxes.

Another misunderstanding involves salary increases. Although additional earnings may increase deductions, employees generally continue earning more overall despite larger withholding amounts.

Payroll deductions can also change during the year because employees update benefit elections, adjust withholding preferences where permitted, receive salary increases, or experience legislative changes affecting payroll systems.

Recognizing these facts encourages more informed conversations between employees, payroll departments, and financial professionals.

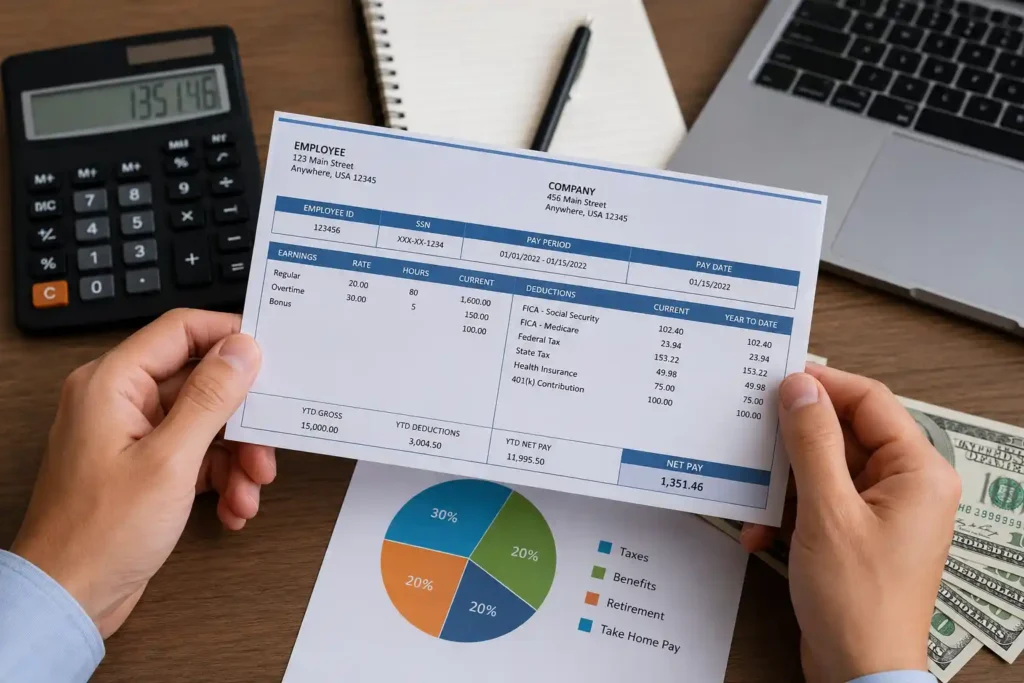

Understanding Your Pay Stub Like a Financial Professional

A pay stub provides considerably more information than simply showing earnings. Learning to interpret every section transforms it into a practical financial planning document.

The earnings section typically displays regular wages, overtime, bonuses, commissions, and total gross pay. The deduction section separates payroll withholding, benefit deductions, retirement contributions, and other adjustments. Many employers also display employer-paid payroll taxes separately for informational purposes.

Year-to-date totals deserve particular attention because they allow employees to monitor cumulative earnings, tax withholding, retirement savings, and benefit contributions throughout the year. Reviewing these figures regularly helps identify payroll errors early before they become more difficult to correct.

The following table highlights how common paycheck deductions support different long-term financial objectives.

| Paycheck Deduction | Mandatory or Optional | Long-Term Purpose |

| Payroll Taxes | Usually mandatory | Fund public programs |

| Income Tax Withholding | Usually mandatory | Meet annual tax obligations |

| Retirement Contributions | Often optional or partially optional | Retirement savings |

| Health Insurance | Often optional depending on employment | Healthcare protection |

| Other Benefits | Usually optional | Financial security and workplace benefits |

Rather than viewing deductions simply as reductions in income, employees should recognize that each represents either compliance with legal requirements or participation in broader financial planning strategies. Reviewing every pay stub carefully also makes budgeting more accurate because employees base spending decisions on actual disposable income instead of gross earnings.

The Future of Payroll and Workplace Finance

Payroll continues evolving alongside digital technology and changing workforce expectations.

Cloud-based payroll platforms increasingly automate payroll withholding, tax calculations, benefit administration, and compliance reporting. Artificial intelligence assists payroll professionals by identifying anomalies, improving accuracy, and reducing administrative workloads.

Real-time payroll systems are also becoming more common in some markets, allowing employees faster access to earned wages while improving payroll transparency. Meanwhile, employers increasingly integrate payroll with broader financial wellness initiatives that encourage budgeting, retirement planning, emergency savings, and employee education.

Automated compliance tools help organizations adapt more quickly when payroll legislation changes. Since payroll tax rules differ across countries and may change regularly, these technologies reduce compliance risks while improving accuracy.

As payroll systems become more transparent, employees gain better access to detailed earnings information, historical records, benefit summaries, and personalized financial insights that support stronger long-term decision-making.

Unique Insight: Payroll Knowledge Is Really Financial Knowledge

Payroll taxes explained is ultimately about much more than understanding deductions. It reflects the relationship between personal financial planning and the broader systems that support retirement funding, healthcare funding, employer compliance, and public services.

Employees who understand payroll deductions typically make better financial decisions because they budget using realistic take-home income rather than gross salary. They also recognize the value of retirement contributions, understand how employee benefits affect overall compensation, and appreciate why employer payroll taxes represent an additional investment beyond visible wages.

Financial literacy often begins with a first paycheck. Carefully reviewing every pay stub helps employees identify payroll errors quickly, monitor benefit elections, understand tax withholding, and track retirement savings throughout their careers.

Perhaps most importantly, paycheck transparency builds confidence. When workers understand where every dollar goes, they become more informed participants in workplace financial decisions while developing stronger long-term personal finance habits.

Frequently Asked Questions

What are payroll taxes?

Payroll taxes are employment-related taxes collected through payroll systems to help fund public programs such as retirement, healthcare, unemployment insurance, or similar government initiatives, depending on the country.

What is the difference between payroll taxes and income tax withholding?

Payroll taxes generally finance employment-related public programs, while income tax withholding represents estimated income taxes collected during the year. They serve different purposes even though both reduce take-home pay.

Why is my net pay lower than my gross pay?

Net pay reflects gross earnings after payroll tax deductions, income tax withholding, retirement contributions, insurance premiums, and other authorized paycheck deductions have been applied.

What payroll taxes do employees typically pay?

Employee payroll taxes vary by jurisdiction but often include employment-related contributions supporting retirement systems, healthcare programs, or similar national benefits.

Do employers also pay payroll taxes?

Yes. Many jurisdictions require employer payroll taxes in addition to employee payroll taxes. These employer-paid amounts usually do not appear as deductions from employee paychecks.

What is included in payroll deductions?

Payroll deductions may include payroll taxes, income tax withholding, retirement contributions, health insurance premiums, charitable deductions, and other voluntary employee benefits depending on employer offerings.

How can I read my pay stub correctly?

Review gross earnings, payroll withholding, benefit deductions, retirement contributions, employer-paid items where shown, and year-to-date totals. Comparing pay stubs regularly helps identify unexpected changes or payroll errors.

Are payroll taxes the same in every country?

No. Payroll tax systems, contribution rates, withholding requirements, employer obligations, and public benefit structures vary significantly between countries and jurisdictions.

Can payroll deductions change during the year?

Yes. Salary adjustments, legislative updates, changes in employee benefits, retirement elections, and withholding preferences may all affect payroll deductions.

Why is Payroll taxes explained important for understanding your paycheck?

Payroll taxes explained helps employees understand why deductions exist, distinguish between taxes and benefits, interpret pay stubs accurately, improve budgeting, and make better long-term personal finance decisions while recognizing that payroll rules differ across jurisdictions.

Administrator at Alt Finances, leading editorial strategy and contributing in-depth coverage of investing, wealth management, alternative assets, and global financial markets. Through research-driven articles and analysis, he helps readers understand the ideas, industries, and market forces shaping modern finance.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}