First-time homebuyer mortgage payment expectations often differ from reality, and many buyers discover the gap only after closing on their new home. While a mortgage calculator may produce an attractive monthly estimate based on the loan amount and interest rate, that figure rarely captures the complete cost of homeownership. As a result, many first-time buyers are surprised when their actual monthly mortgage payment turns out to be significantly higher than anticipated.

The difference stems from more than the loan itself. Property taxes, homeowners insurance, private mortgage insurance (PMI), escrow requirements, homeowners association (HOA) fees, and ongoing maintenance all contribute to monthly housing expenses. At the same time, rising insurance premiums, increasing tax assessments, and broader affordability challenges have made accurate budgeting more important than ever.

Buying a home remains one of the largest financial commitments most people will ever make. Yet many prospective homeowners understandably focus on qualifying for a mortgage instead of evaluating the full range of recurring ownership costs. This disconnect can create unnecessary financial stress during the first months of homeownership, particularly when buyers have not planned for expenses beyond principal and interest.

Understanding how every component of a mortgage payment works helps buyers make more informed decisions before signing a loan agreement. While actual costs vary depending on location, loan type, down payment, insurance requirements, and local taxes, evaluating the complete monthly obligation—not just the advertised mortgage payment—provides a much clearer picture of long-term affordability.

Understanding What Makes Up a Monthly Mortgage Payment?

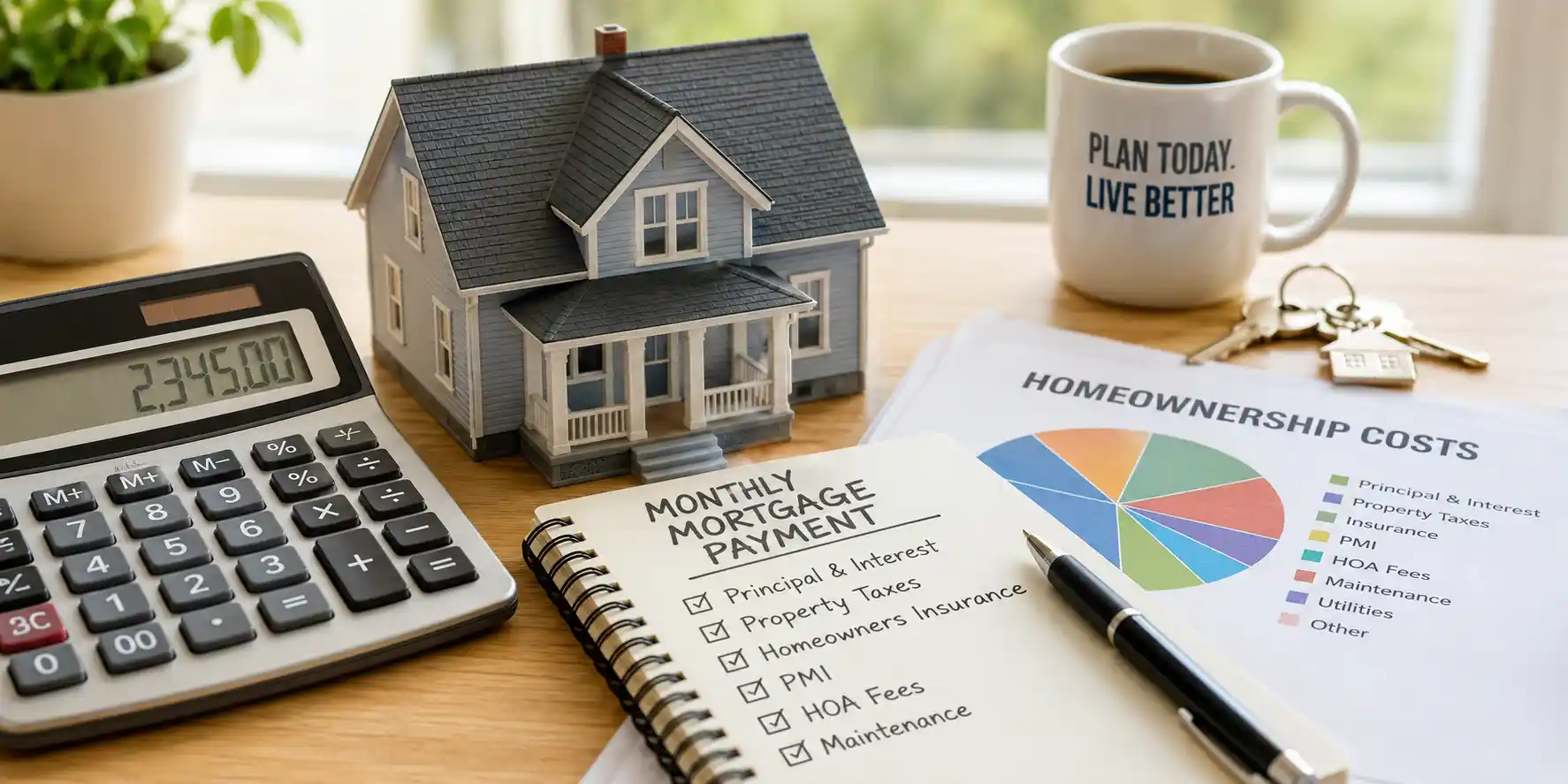

Many first-time buyers assume that a mortgage payment consists solely of repaying the money borrowed from the lender. In reality, the payment is typically made up of several different components, each serving a specific purpose. Understanding these elements is essential for building a realistic housing budget.

The foundation of every mortgage payment is principal and interest.

The principal represents the amount borrowed to purchase the home. Every monthly payment gradually reduces this balance until the loan is fully repaid. Interest, meanwhile, is the cost of borrowing money and is calculated according to the loan’s interest rate and remaining balance.

During the early years of many mortgages, a larger portion of each payment goes toward interest rather than principal. Over time, that balance shifts, allowing homeowners to build equity more quickly.

However, principal and interest often account for only part of the monthly payment.

Most lenders also require borrowers to contribute toward property taxes and homeowners insurance through an escrow account. Rather than paying these bills separately when they become due, homeowners make monthly contributions that the lender collects and later distributes on their behalf.

This arrangement benefits both parties. Homeowners spread large annual expenses across the year, while lenders reduce the risk that taxes or insurance premiums go unpaid.

For many first-time homebuyers, another important expense is Private Mortgage Insurance (PMI).

PMI generally applies when a buyer makes a down payment of less than 20 percent. Although it protects the lender rather than the homeowner, the borrower usually pays the monthly premium until sufficient home equity has been built or other loan requirements are met.

Some homeowners also pay HOA fees if they purchase property within a managed community or condominium association. These fees help maintain shared amenities and common areas but can substantially increase monthly housing costs depending on the neighborhood.

Beyond these recurring charges, homeowners should also prepare for expenses that rarely appear in mortgage documents.

Common ownership costs include:

- Utility bills such as electricity, water, gas, and internet.

- Routine maintenance, including landscaping, HVAC servicing, and appliance repairs.

- Unexpected repairs for roofing, plumbing, or electrical systems.

- Seasonal maintenance and long-term home improvements.

Although these expenses are separate from the lender’s monthly payment, they remain an unavoidable part of responsible homeownership.

The key takeaway is that the true monthly cost of owning a home extends well beyond the loan itself. Buyers who understand every component before purchasing are far less likely to experience financial surprises after moving in. Viewing the mortgage as only one part of a broader housing budget creates a stronger foundation for sustainable long-term ownership.

Why Mortgage Calculators Often Underestimate Monthly Costs?

Online mortgage calculators have become one of the most popular tools for prospective buyers because they provide quick estimates of affordability. By entering a purchase price, down payment, loan term, and interest rate, users receive an estimated monthly payment within seconds.

While these calculators are useful starting points, they often present a simplified version of reality.

Many basic calculators focus primarily on principal and interest while relying on estimated assumptions—or excluding entirely—other expenses that significantly affect the final payment. Consequently, buyers may believe they can comfortably afford a home based on an incomplete picture of their future financial obligations.

One major source of variation is property taxes.

Tax rates differ not only between states but also between counties, cities, school districts, and even individual neighborhoods. A modest difference in local tax assessments can translate into hundreds of dollars each month, making generic calculator assumptions far less accurate than property-specific estimates.

Insurance introduces another layer of uncertainty.

Homeowners insurance premiums depend on numerous factors, including the home’s location, replacement cost, construction materials, claims history, weather risks, and available coverage options. In regions exposed to hurricanes, floods, wildfires, or severe storms, insurance costs may rise significantly over time, increasing the overall monthly payment.

Loan structure also affects affordability.

Buyers making smaller down payments often pay PMI, while certain loan programs may include additional insurance premiums or guarantee fees. These costs vary by lender and loan type, meaning two buyers purchasing similarly priced homes may have noticeably different monthly obligations.

Community-related expenses are another commonly overlooked factor.

Properties governed by homeowners associations frequently charge monthly or quarterly HOA fees that cover shared amenities, maintenance, security, or neighborhood services. Since these charges are not part of every home purchase, many online calculators exclude them unless users manually enter the information.

Even when calculators include taxes and insurance, they cannot anticipate future changes.

Property taxes may increase following reassessments, insurance premiums can rise due to inflation or climate-related risks, and escrow payments are periodically adjusted to reflect actual expenses. As a result, a homeowner’s monthly payment can change over time even if the loan’s principal and interest remain fixed.

For that reason, buyers should treat mortgage calculators as planning tools rather than precise forecasts. They provide valuable guidance during the early stages of a home search, but they cannot fully account for every local, financial, and property-specific variable.

The most financially prepared homeowners look beyond the headline payment and evaluate the complete cost of ownership before making an offer. That broader perspective supports better mortgage affordability, reduces unexpected expenses after closing, and ultimately leads to more confident long-term homeownership decisions.

The Monthly Costs Beyond Principal and Interest

Once buyers understand the mechanics of a mortgage loan, the next step is recognizing the ongoing expenses that shape the true cost of homeownership. These recurring costs often explain why the actual First-time homebuyer mortgage payment exceeds the estimate generated by a basic calculator.

Property taxes are among the largest additional expenses. Local governments use these taxes to fund schools, public infrastructure, emergency services, and community programs. Because tax rates vary by location and assessed property value, two similar homes in different neighborhoods can produce very different monthly obligations.

Homeowners insurance is another essential cost. Most mortgage lenders require borrowers to maintain adequate coverage throughout the life of the loan. Insurance premiums depend on factors such as the home’s value, construction, location, weather risks, and policy coverage, making them difficult to estimate with complete accuracy.

For buyers who make a smaller down payment, PMI increases monthly housing expenses until sufficient equity is built. Although PMI eventually ends under qualifying conditions, it can represent a meaningful portion of the monthly budget during the early years of homeownership.

Some neighborhoods also require HOA fees, which fund maintenance of common areas, landscaping, amenities, and community services. While these fees can enhance property values and neighborhood upkeep, they should always be included when evaluating affordability.

Finally, homeowners must prepare for utilities and maintenance. Unlike renters, homeowners are responsible for routine repairs, appliance replacement, HVAC servicing, plumbing issues, and countless other ownership expenses that arise over time.

The table below illustrates which costs are commonly included in basic mortgage calculators and why each expense matters.

| Monthly Housing Expense | Included in Basic Mortgage Calculator? | Purpose |

|---|---|---|

| Principal & Interest | Yes | Repays the loan balance and borrowing cost |

| Property Taxes | Sometimes | Funds local government services |

| Homeowners Insurance | Sometimes | Protects the home against covered losses |

| PMI | Often omitted unless specified | Protects the lender when the down payment is low |

| HOA Fees | Usually No | Supports community maintenance and shared amenities |

| Utilities & Maintenance | No | Covers ongoing ownership and property upkeep |

This comparison demonstrates why relying solely on a mortgage estimate can create unrealistic expectations. Even when the loan payment appears affordable, the complete monthly housing budget may be considerably higher after accounting for taxes, insurance, and ownership responsibilities. Evaluating these costs before purchasing helps buyers avoid financial surprises and make more sustainable long-term decisions.

Budgeting for Sustainable Homeownership

Affording a home involves far more than qualifying for a mortgage. Successful homeowners build financial flexibility into their budgets so they can manage both expected expenses and unexpected repairs without placing unnecessary strain on their finances.

A practical mortgage budgeting strategy typically includes:

- Maintaining an emergency savings fund for unexpected home repairs.

- Setting aside monthly savings for routine maintenance and future replacements.

- Reviewing annual insurance and tax changes as part of the household budget.

- Accounting for inflation, which may increase maintenance and utility costs over time.

- Leaving room in the budget for changing family or lifestyle needs.

Housing affordability also depends on recognizing that ownership costs rarely remain static. Property tax assessments can rise, insurance premiums may increase, and aging homes naturally require additional maintenance. Buyers who budget only for today’s payment may find future adjustments more difficult to absorb.

Instead, viewing homeownership as an ongoing financial commitment encourages better planning and greater long-term stability. Responsible budgeting helps homeowners enjoy the benefits of owning property while reducing the likelihood that unexpected expenses become financial setbacks.

Comparing Mortgage Payments With Total Housing Costs

Many buyers focus on the monthly payment shown on their loan documents, yet the broader housing budget provides a more accurate picture of affordability. Comparing each major expense category highlights why evaluating total ownership costs is more valuable than looking only at principal and interest.

| Housing Cost | Short-Term Impact | Long-Term Budget Importance |

|---|---|---|

| Principal & Interest | Predictable monthly payment | Builds home equity over time |

| Taxes & Insurance | Moderate to high; may change annually | Essential recurring ownership expense |

| PMI & HOA Fees | Can significantly increase monthly costs | May decrease or change depending on circumstances |

| Maintenance & Utilities | Often varies month to month | Critical for preserving the home’s value and financial stability |

Principal and interest generally remain the most predictable portion of the housing budget for borrowers with fixed-rate mortgages. By contrast, taxes, insurance, and maintenance costs can change over time, making long-term planning especially important.

Maintenance deserves particular attention because it is frequently underestimated. Even newer homes require routine servicing, while older properties may demand larger investments in roofing, plumbing, heating systems, or structural repairs. Setting aside funds each month helps reduce the financial impact when these expenses eventually arise.

Beyond the obvious monthly expenses, homeowners should also plan for hidden costs such as appliance replacements, emergency repairs, landscaping, pest control, moving expenses, and occasional renovation projects, all of which can have a meaningful impact on the overall cost of homeownership.

Looking at total housing costs instead of only the mortgage payment gives buyers a more realistic understanding of affordability and encourages stronger financial decision-making throughout the life of the loan.

The Future of Homeownership Affordability

Homeownership continues to evolve alongside broader economic and housing trends. Rising insurance premiums, higher construction costs, climate-related risks, and increasing property taxes are influencing the long-term affordability of owning a home in many regions.

At the same time, technology is improving financial planning. Modern budgeting platforms, more advanced mortgage calculators, and digital financial management tools help buyers estimate recurring expenses more accurately than ever before. Although no calculator can predict every property-specific cost, these tools encourage more informed purchasing decisions.

Lenders are also placing greater emphasis on responsible borrowing, ensuring that applicants understand both their loan obligations and their broader housing expenses. As affordability challenges persist, comprehensive budgeting is becoming just as important as securing a competitive interest rate.

Ultimately, successful homeownership will depend not only on financing a purchase but also on managing the recurring costs that accompany owning a property over many years.

Unique Insight

The First-time homebuyer mortgage payment should never be viewed as the complete monthly cost of owning a home. Instead, it represents just one component of a much broader financial commitment that includes taxes, insurance, maintenance, utilities, and other recurring expenses.

Buyers who plan for these ongoing costs often experience greater financial stability because they are less likely to be surprised by annual tax increases, higher insurance premiums, or unexpected repairs. Likewise, while a mortgage calculator provides a valuable starting point, it cannot fully account for local tax policies, property-specific insurance requirements, HOA fees, or future maintenance needs.

The most confident homeowners typically evaluate their entire monthly housing budget rather than focusing solely on the mortgage payment. As housing affordability continues to evolve, understanding the complete cost of ownership will remain one of the most important factors in making sustainable, informed home-buying decisions.

Frequently Asked Questions

What is included in a monthly mortgage payment?

A monthly mortgage payment commonly includes principal, interest, property taxes, homeowners insurance, and, when required, PMI through an escrow account. Some homeowners also pay HOA fees separately.

Why is my actual mortgage payment higher than the calculator estimate?

Basic mortgage calculators may exclude or estimate expenses such as property taxes, homeowners insurance, PMI, HOA fees, or escrow adjustments, resulting in lower estimated payments than actual costs.

What is an escrow account?

An escrow account is managed by the lender to collect monthly funds for property taxes and homeowners insurance before those bills become due.

Does homeowners insurance increase my monthly payment?

Yes. When insurance premiums are paid through escrow, they become part of the total monthly mortgage payment.

What is private mortgage insurance (PMI)?

PMI protects the lender if the borrower defaults on the loan. It is commonly required when the down payment is less than 20% and increases monthly housing costs.

Do HOA fees count as housing expenses?

Yes. HOA fees are recurring housing expenses and should always be included when calculating the total monthly cost of owning a home.

How much should homeowners budget for maintenance?

While the exact amount varies by the property’s age, condition, and location, homeowners should consistently reserve money for routine maintenance and unexpected repairs.

Can property taxes change over time?

Yes. Property taxes may increase because of reassessments, local tax rate changes, or rising property values, which can affect monthly escrow payments.

How can first-time buyers estimate total monthly housing costs?

Buyers should combine principal, interest, property taxes, homeowners insurance, PMI, HOA fees, utilities, maintenance, and other recurring expenses rather than relying solely on a basic mortgage calculator.

Why is First-time homebuyer mortgage payment often higher than expected?

A First-time homebuyer mortgage payment is often higher than expected because buyers frequently focus on principal and interest while overlooking taxes, insurance, escrow, PMI, HOA fees, and ongoing homeownership costs that substantially increase the total monthly housing budget.

Administrator at Alt Finances, leading editorial strategy and contributing in-depth coverage of investing, wealth management, alternative assets, and global financial markets. Through research-driven articles and analysis, he helps readers understand the ideas, industries, and market forces shaping modern finance.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}