High-yield savings accounts are among the most effective tools for growing your savings without taking on investment risk. These accounts offer significantly higher interest rates than traditional savings accounts, making them an ideal option for emergency funds, short-term goals, or simply earning more on your idle cash.

In this comprehensive guide, we compare the best high-yield savings accounts in 2025, examine their features, and help you determine which one suits your financial needs.

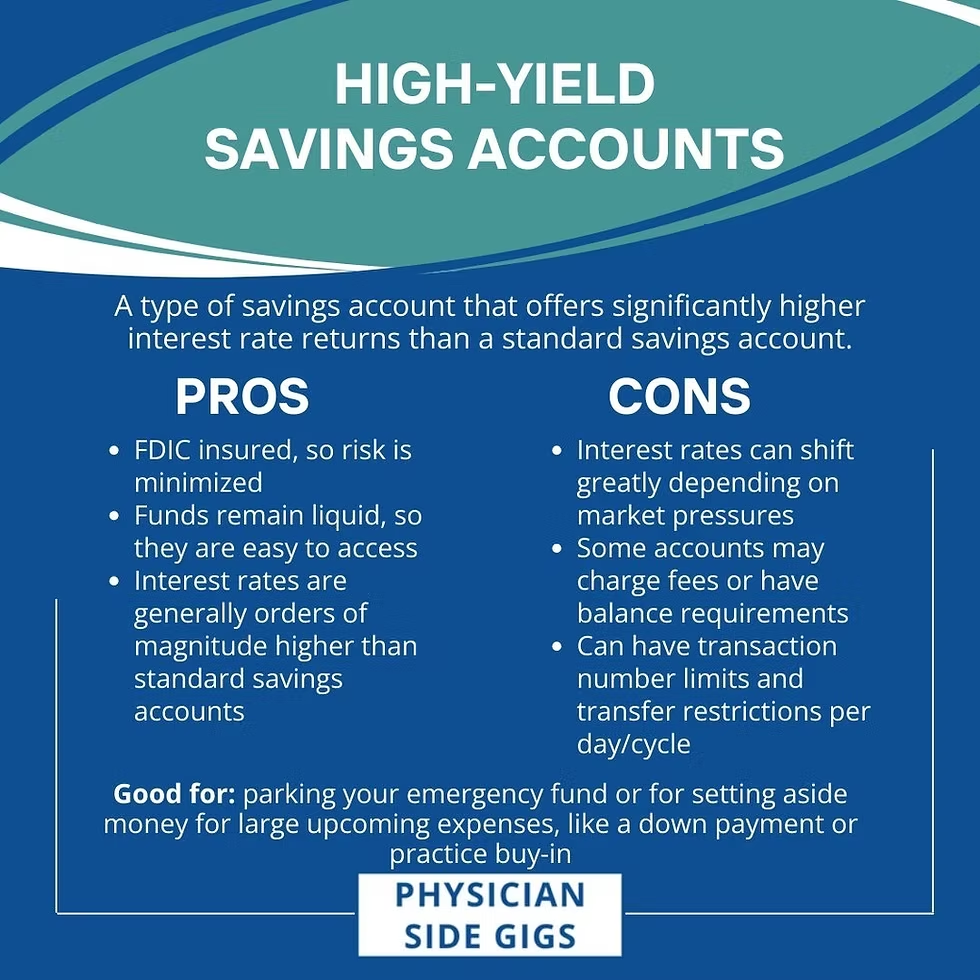

What Is a High-Yield Savings Account?

A high-yield savings account (HYSA) is a type of federally insured deposit account that pays interest rates far above the national average. Unlike regular savings accounts, which may offer interest rates as low as 0.01%, HYSAs typically offer APYs ranging from 4% to 5% or higher (as of 2025).

These accounts are usually offered by online banks, credit unions, and some traditional institutions looking to stay competitive. They often come with low or no fees and minimal balance requirements.

Benefits of High-Yield Savings Accounts

Higher Returns: Earn more interest on your savings than with a traditional account.

FDIC/NCUA Insurance: Funds are insured up to $250,000.

Low Risk: Virtually no risk of losing your money.

Flexibility: Easy access to funds, especially with online and mobile banking.

Great for Financial Goals: Perfect for saving for emergencies, vacations, or down payments.

Top High-Yield Savings Accounts in 2025

The table below compares some of the top-performing high-yield savings accounts based on APY, fees, and features.

Table: Best High-Yield Savings Accounts (2025)

| Bank/Institution | APY (%) | Minimum Balance | Monthly Fees | Unique Features |

|---|---|---|---|---|

| Ally Bank | 4.35% | $0 | $0 | Auto-savings tools, 24/7 support |

| Marcus by Goldman Sachs | 4.40% | $0 | $0 | High APY, user-friendly mobile app |

| Synchrony Bank | 4.50% | $0 | $0 | ATM access, optional check-writing |

| SoFi | 4.60% | $0 | $0 | Offers cash back, automatic savings vaults |

| Discover Online Savings | 4.25% | $0 | $0 | Reliable brand, fee-free overdraft protection |

| American Express® Bank | 4.30% | $0 | $0 | Simple interface, trusted reputation |

How to Choose the Best High-Yield Savings Account

1. Interest Rate (APY)

The higher the annual percentage yield (APY), the faster your money grows. Compare rates regularly, as they may change based on the Federal Reserve’s monetary policy.

2. Fees

Avoid accounts with maintenance or withdrawal fees. Most top HYSAs now offer zero monthly fees.

3. Accessibility

Choose an account that offers easy transfers, mobile apps, and possibly ATM access if you want to withdraw funds occasionally.

4. Customer Service

Read reviews and consider institutions with responsive customer support. Online banks typically offer 24/7 service through chat or phone.

5. Features

Some banks offer tools to help you automate savings, budget your income, or create savings “buckets” for specific goals.

How Much Can You Earn?

Here’s an example of potential earnings from a high-yield savings account:

If you deposit $10,000 into an account with a 4.50% APY, compounded monthly, you would earn approximately $450 in interest over 12 months—significantly more than a traditional account offering only 0.05% ($5 per year).

High-Yield Savings vs Other Options

| Account Type | Average APY | Liquidity | Risk Level | Ideal For |

|---|---|---|---|---|

| High-Yield Savings | 4.25%-4.60% | High | Low | Emergency funds, short-term savings |

| Money Market Account | 3.50%-4.00% | High | Low | Higher balances, check-writing |

| CDs (1-Year) | 4.50%-5.00% | Low | Low | Fixed terms, fixed interest |

| Traditional Savings | 0.01%-0.10% | High | Low | Basic storage of funds |

Related Consideration: Education and Savings

People saving for education-related goals—such as tuition, online courses, or student loan repayment—may consider pairing their HYSA with educational programs or forgiveness initiatives. One such relevant topic in 2025 is the Student loan forgiveness programs 2025, which may impact how much individuals need to save or repay depending on eligibility. Understanding these options can help in better financial planning and use of savings accounts as a buffer or supplement.

FAQs: High-Yield Savings Accounts

1. Are high-yield savings accounts safe?

Yes. These accounts are insured by the FDIC (banks) or NCUA (credit unions) up to $250,000, protecting your funds from loss.

2. Can I lose money in a high-yield savings account?

No. These accounts do not involve investment risk, and your balance never decreases unless you withdraw funds.

3. Are online banks better for high-yield savings?

Often, yes. Online banks have fewer overhead costs and can pass those savings to customers through higher APYs.

4. Is there a catch with high APYs?

Usually not, but be sure to read the fine print. Some rates are promotional and may drop after a few months. Also, ensure there are no minimum balance requirements that trigger fees.

5. How often do interest rates change?

Interest rates on high-yield savings accounts are variable and can change at any time based on economic conditions, especially changes in the Federal Reserve rate.

6. Can I withdraw money anytime?

Yes. High-yield savings accounts offer easy access to funds. However, some banks may limit the number of withdrawals per month to comply with federal regulations.

7. What’s the difference between a high-yield savings account and a CD?

A CD (Certificate of Deposit) locks in your money for a fixed term, often at a slightly higher rate. HYSAs allow you to access your money anytime but offer variable interest.

Final Thoughts

High-yield savings accounts in 2025 offer a safe, flexible, and rewarding way to grow your money. With APYs often above 4%, these accounts are perfect for emergency funds, short-term savings goals, or simply earning more on your unused cash. Whether you prioritize customer service, digital tools, or maximum interest rates, there’s a HYSA to fit your needs.

Always compare account details, track rate changes, and consider how your savings strategy fits into your broader financial picture, including debt, investments, and potential support from evolving policies like Student loan forgiveness programs 2025.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}